When you take a loan, you pay an EMI for the loan at a specific rate of interest, which is the bank’s rate of return. Similarly, when you invest in a home and lease it to a tenant, the returns you get are the monthly rent and the final underlying asset value. So, each investment has a certain future cash flow and a current cost which determines the worthiness of that investment. When an investor or a company invests in a project, the future cash flows from the project determine whether it is worth the investment or not. For the investor or the company, the rate of return should always be higher than the interest rate (in the case of debt) that he is paying for the money invested or the opportunity cost for the money invested (other attractive investments). In essence, the rate of return from a project should be more than the cost of capital invested in the project, only then will you get some profit from the project.

So, how do you determine what is the cost of capital for the individual or firm?

A firm or an individual can have loans or debt from various sources at various interest rates (cost of capital). So, there should be a weighted cost of capital (weighted rate of interest). Similarly, a firm or an individual may not have only debt as a source of money; money would’ve been raised in the form of equity. So, the cost of capital calculation should take into consideration both debt and equity. Below is the popular fomula of the weighted average cost of capital (WACC):

While the cost of debt is the interest rate paid for the debt, it is very complicated to know the cost of capital for equity money. When an investor invests in a company in the form of equity, the investor gets the return in the form of shares of the company (company pays the cost of capital of equity in the form of dilution) and the investor doesn’t get any guaranteed cash in-flow whereas in the case of debt there is a guaranteed incoming of cash-flow. This makes it very difficult to measure the cost of capital for a company raising equity money whereas when you are taking debt the cost of capital is the interest rate of debt.

How do you measure the cost of capital for equity?

This confusion in quantifying the cost of capital for equity investment has raised a huge requirement for academic research in this area. There are now multiple models to measure the cost of capital for equity money (also called the cost of equity).

Equity investors contribute equity capital with the expectation of getting a return at some point down the road. The riskier future cash flows are expected to be, the higher the returns that will be expected. The capital asset pricing model (CAPM) is a popular framework for measuring the cost of equity.

The CAPM divides risk into two components:

- Unsystematic (company-specific) risk: Risk that can be diversified away (so ignore this risk).

- Systematic risk: The company’s sensitivity to market risk can’t be diversified away, so investors will demand returns for assuming this risk.

Since the CAPM essentially ignores any company-specific risk, the calculation for cost of equity is simply tied to the company’s sensitivity to the market. The formula for quantifying this sensitivity is as follows.

Cost of equity formula

Cost of equity = Risk free rate +[β x ERP]

- β (“beta”) = A company’s sensitivity to systematic risk

- ERP (“Equity risk premium”) = The incremental risk of investing in equities over risk free securities

The risk-free rate

The risk-free rate should reflect the return of a default-free government bond or fixed deposit of equivalent maturity to the duration of each cash flow being discounted. In India, a fixed deposit yields around 4.5% return in the future time.

How much extra return above the risk-free rate do investors expect for investing in equities in general?

For example, if you plan to invest in the S&P 500 — a proxy for the overall stock market — what kind of return do you expect? Certainly you expect more than the return on U.S. treasuries, otherwise why take the risk of investing in the stock market? This additional expected return that investors expect to achieve by investing broadly in equities is called the equity risk premium (ERP) or the market risk premium (MRP).

But how is that risk quantified? The prevalent approach is to look backward and compare historical spreads between S&P 500 returns and the yield on 10-yr treasuries over the last several decades. The logic being that investors develop their return expectations based on how the stock market has performed in the past. The ERP usually ranges from 4-6%.

The S&P CNX Nifty is a free float capitalization-weighted index that tracks 50 Indian blue-chip stocks (market cap over 5 billion Indian rupees) and covers approximately 60% of the National Stock Exchange of India’s market cap.** NASDAQ: INDY tracks this.

The BSE Sensex is a free float capitalization-weighted index that tracks 30 Indian stocks and covers approximately half of the Bombay Stock Exchange’s market cap.

The BSE 500 is a free float capitalization-weighted index that tracks 500 Indian stocks and covers approximately 93% of the Bombay Stock Exchange’s market cap.

Benchmark index of BSE in India- Sensex

Benchmark index of NSE in India- Nifty

Sensex has provided a 14.7% CAGR since 1970. Sensex is an index and not a company, therefore, one cannot buy a share of Sensex but one can buy a future of Sensex. One can invest in Sensex by buying ETF, UTI and HDFC have Sensex ETF.

Calculating beta

The final calculation in the cost of equity is beta. It is the only company-specific variable in the CAPM. Beta in the CAPM seeks to quantify a company’s expected sensitivity to market changes. For example, a company with a beta of 1 would expect to see future returns in line with the overall stock market.

Meanwhile, a company with a beta of 2 would expect to see returns rise or fall twice as fast as the market. In other words, if the S&P were to drop by 5%, a company with a beta of 2 would expect to see a 10% drop in its stock price because of its high sensitivity to market fluctuations.

The higher the beta, the higher the cost of equity, because the increased risk investors take (via higher sensitivity to market fluctuations), should be compensated via a higher return.

“Beta” for any stock is basically it’s “elasticity” as compared with that of the Sensex. Basically, it means that how a stock is expected to behave over a long run as compared with the increase or decrease in Sensex prices. So, a 1.8 beta stock should ideally grow by 1.8% when the Sensex grows by 1% in the long term while it will decrease also by 1.8% if the Sensex decreases by 1% only.

High beta stocks are generally considered much riskier but can also provide much better returns in upside while Low Beta Stocks are generally considered as defensive stocks which are very important for the safety of the portfolio and initial corpus. High beta is mostly perceived as high risk, high reward stocks.

Real estate, banks, NBFCs etc are considered high beta stocks while that of FMCG, Pharma etc are considered low beta stocks.

In the case of bullish trends, people tend to buy more high beta shares while in case of the undecided or bearish market, it’s always safer to take shelter under the umbrella of low beta stocks.

Calculating raw (historical) beta

How do investors quantify the expected future sensitivity of the company to the overall market? Just as with the estimation of the equity risk premium, the prevailing approach looks to the past to guide expected future sensitivity. For example, if a company has seen historical stock returns in line with the overall stock market, that would make for a beta of 1. You would use this historical beta as your estimate in the WACC formula.

Companies such as Bloomberg, Standard & Poor (S&P) and Barra publish the Beta values for various stocks basis historical analysis.

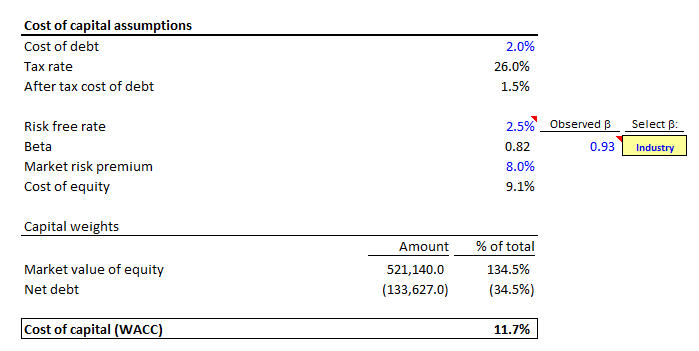

Overall weighted average cost of capital (WACC)

The overall weighted average cost of capital for a company is:

r (debt) is usually the rate of interest

r (equity) is equal to Risk free rate +[β x ERP] (as mentioned above earlier)

Example of calculation of Apple’s WACC:

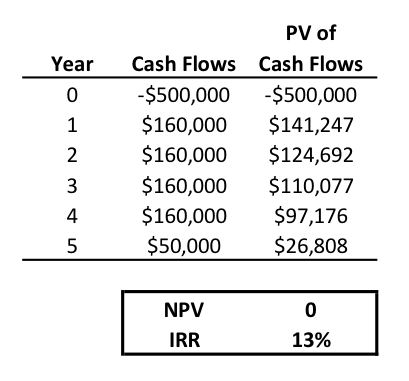

Internal Rate of Return (IRR)

IRR is the rate of return expected from any investment. It is calculated as the discount rate that makes the present value of the cash inflows equal to the present value of the cash outflows in a capital budgeting analysis. Therefore, if the IRR for a potential investment is lower than your cost of capital, then you should reject that investment.

A company is deciding whether to purchase new equipment that costs $500,000. Management estimates the life of the new asset to be 4 years and expects it to generate an additional $160,000 of annual profits. In the 5th year, the company plans to sell the equipment for its salvage value of $50,000.

Internal Rate of Return is widely used in analyzing investments for private equity and venture capital, which involves multiple cash investments over the life of the business and a cash flow at the end through an IPO.

Hope this is useful, thanks!

Source (s):

https://hbr.org/2012/07/do-you-know-your-cost-of-capital

You must be logged in to post a comment.