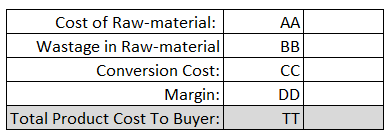

When you talk to manufacturers, they frequently use a term called ‘conversion costs’ and a few of them also use the term ‘Prime Costs’ (especially used by Chinese vendors). A typical manufacturer would look at charging you as below:

So, you could guess: Conversion Cost is the total cost that is borne by the manufacturer to convert the raw-material into finished goods. It includes all manufacturing costs except the raw-material cost i.e. all direct labor costs and manufacturing overheads. Prime Costs are all the costs that can be associated directly with the production of a unit, it comprises of all direct material costs and direct labor costs.

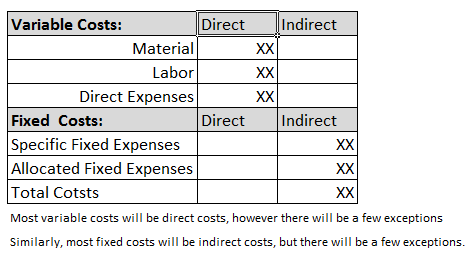

Typically, there are costs that are involved in the production of finished goods directly such as raw-material and costs that are not directly involved in the production of finished goods such as building rent. Therefore, there are direct costs and indirect costs. Usually, direct costs are variable costs in proportion to the production volume and indirect costs are usually fixed costs such as rent, electricity, etc. However, there can be exceptions sometimes.

Prime costs = direct materials cost + direct labor cost

Conversion costs = direct labor cost + manufacturing overhead costs

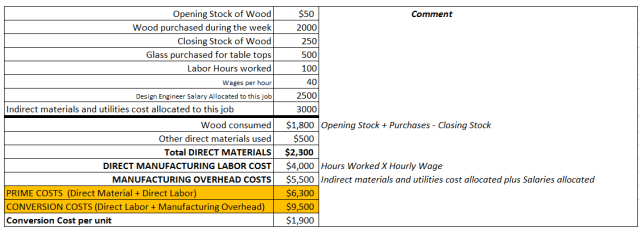

Example:

Chesters Furniture is a small furniture manufacturer. In the first week of June, they worked exclusively on an order to build 5 study tables.

Costs incurred are in the first half of the table, and the calculation of conversion costs are in the second half of the table.

Another Example of Calculation of Conversion Costs:

Most manufacturers in the furniture industry work basis the Gross Profit (GP) % = (Selling Price – Bill of Materials)/(Selling Price). So, if your Bill of Material for a product (including the bigger raw-material such as wood, hardware and the smaller raw-material such as gum, consummables, etc.) is Rs.5000 and the end product is sold by the manufacturer at Rs.9000 then the GP% is 44% (9000-5000)//9000.

Typically, manufacturers will charge different GP% for different customers depending on the volume of the business. For a large volume long-term customer, the manufacturer might charge only 20% GP whereas for a small customer who hasn’t built the trust and the relationship yet might be charged 45% GP.

Also, manufacturers don’t usually work on each of the product costing separately basis the amount of time it is taking on different types of machines etc. They have category wise rough GP estimates that they use as their main source of calculation. For example, if the product needs drilling machine but not the routing machine then the GP% is taken in one way and if the product needs drilling + routing then the GP% is different. Similarly, if it is horizontal drill alone it is a different GP% and if it is both horizontal + vertical drill the GP% is different. Similarly, if a beam saw is used, then the GP% is different (possibly lower) because it is automatic program based machine that doesn’t need labor. Whereas a panel saw machine will need one technician and one helper to turn the panel and to set it, so the GP% will be different. But, generally, they work at a higher level of GP for each category of products as a certain category of products require certain types of machines only, and hence the GP% is usually set by manufacturers at product-type level. For example, beds will have a certain x% of GP whereas Study Tables will have a Y% of GP. But, eventually, if you drill down the costing, you might get some cost efficiencies.

| Beam Saw Machine |

| Vertical & Horizontal Drilling Machine |

| Routing Machine |

| Edgebanding Machine |

| Panel Saw Machine |

Some of the solid-wood toolds are: planer, hand circular saw, hydraulic chisel machine, doweling jig, CNC router, etc.

Refer to this video to see the solid-wood working tools: https://www.youtube.com/watch?v=KLsFMVsQQyU

So, the costing department in manufacturing will first take out all the Bill Of Material (BOM) including how many panels are required, how many membrane panels are required, how much wood is required, size wise, and then the hardware cost and other costs are taken into consideration. Once you get this full cost, then they typically apply a GP% over that applicable for that particular category. But, the sales team can bring down the GP% for a customer who is important.

Once the design reeaches the manufacturer, the manufacturer starts making the cutting plan, drilling plan and floor plan for the product. A lot of this is even automated and the logic is already programmed in AutoCAD enabled systems or sometime it is done manually.

Hope this is helpful, thank you.

You must be logged in to post a comment.