Knowing the overhead costs is essential to any manufacturer in calculating the total cost of manufacturing of a product and hence to set a profitable selling price. The buyer should always know what is the overhead cost and indirect cost included in the product as a percentage of the cost of the product that the manufacturer is considering. Most suppliers across will say “Sir, please give us some advance, because if I take loan or overdraft account, the overheads are already over the roof. And we will offset the amount in purchase orders. ” The smartie doesn’t want to understand that everyone has a cost of capital.

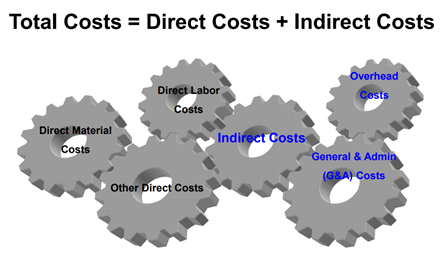

As most of us know, direct costs are costs that can be tied to one cost objective. In making a particular product say a sofa, you will have direct material such as wood, foam, springs, belts, adhesives, and fabric and direct labor that is used in creating that particular product specifically. Other direct costs would be such costs that are one-time significant expenses incurred and the benefit of that can only be attributed to one firm’s products and therefore it will be unfair to other firms to treat it as an indirect cost and allocate it to all. For example, for a particular product of a customer firm a specific testing tool to test the quality of the product (say load testing of a specific foam only used for one customer) is needed. This testing tool is actually not in the direct material of the product, but this testing tool is required for the testing of only a particular firm’s products. So, it is still a direct cost for the firm’s products but not in direct material (DM) or direct labor (DL).

Indirect costs are costs that cannot be tied to one cost objective, but can be tied to multiple (two or more) cost objectives. Indirect costs broadly come in two types: Overheads and G&A. Overheads are still costs that support the production of goods in some way. For example, the electricity that is required to run the machines that produce output goods. Electricity is still some way a direct cost, but not directly producing the good. Overheads are defined as those indirect support costs incurred to support operations or direct production. These are costs directly related to projects but cannot be identified to one project or contract. A good example is operations management where functions support the overall operation. Another is depreciation of equipment used on projects but not exclusively identifiable to one. Quality assurance is another. Supplies (such as hardware) used or consumed in a process but not identifiable to one project or contract. In summary it is related to the operation or production but not identifiable to one project, contract, order or product. On the other hand, there are some costs that are not involved in making any goods such as the electricity cost of the air-conditioning of the staff office or the salary of the accounts staff. These are the support costs that allow the business to function and that can be marked as General & Adminstrative (G&A).

Typically, if you meet a manufacturer (sometimes called as vendor), he or she will include the below in overheads usually:

- Indirect labor

- G& A (Salary)

- Factory Maintenance Charges

- Machine Maintenance Charges

- Bank Interest Charges

- Transportation charges of inbound raw-materials

- Additional 10% buffer for floating capital of operations

Even if the vendor doesn’t have any orders in a month, the vendor will still incur about 12-15% overhead expenses, and he will try to pass that to the buyer in some manner. Therefore, it is always important to understand the overhead expenses of a manufacturer as a percentage of revenue and as a percentage of direct labor.

- Overhead Costs as a percentage of direct labor

- Overhead Costs as a percentage of revenue

In the industry, when you are discussing with vendors (or manufacturers) the way they deal with indirect costs and what they consider under what head will be a little different. This is where the vendor manager needs to understand the supplier in how they consider internally the varios indirect costs and the cost of financing.

Read this post to understand the prime costs and conversion costs of a manufacturer.

Read the below pdf to further understand in depth and with examples.

Pingback: Indirect Costs, Marginal Cost, Marginal Revenue, and Quantity Discounts – Supplier & Buyer Views – Brandalyzer